Which Is Better: Gold or Paper Money? A Complete Analysis

For centuries, the question of gold versus paper money has shaped views on preserving wealth, especially during inflation and market instability. Gold and paper money serve different purposes. Gold is a tangible, limited asset, while paper money is flexible and supports everyday commerce. Understanding these differences can help investors make more informed decisions about protecting purchasing power over time.

This analysis compares gold and fiat currency across historical performance, inflation protection, practical use and long-term wealth preservation. Whether you are considering gold vs. paper money for your portfolio or seeking to view gold as an inflation hedge, this guide offers the insight you need.

Understanding Money: From Gold Standards to Modern Currency

Money has three main functions — it acts as a medium of exchange, a unit of account and a store of value. Different forms of money have fulfilled these roles with varying success throughout history.

To understand the risks facing modern savings, you should first understand the history of the gold standard and how the money in your wallet has changed over the last century.

The Historical Relationship Between Gold and Paper Money

For much of recorded history, gold served as money itself or as backing for paper currency. Under gold-backed systems, paper notes represented a claim on a specific amount of gold held by governments or central banks. This setup limited how much currency could be issued and connected monetary value to a physical asset.

Gold’s durability, scarcity and near-universal acceptance made it a trusted store of value across different cultures. Even as paper currency emerged, its credibility often relied on its convertibility into gold.

Why Countries Abandoned the Gold Standard

During the 20th century, many countries ended the gold standard to gain more control over their monetary policy. Tying currency issuance directly to gold reserves made it harder for governments to respond to economic crises, wars and recessions.

The U.S. ended gold convertibility in 1970, shifting to a fiat currency system managed by the Federal Reserve. By 1973, most major economies also abandoned the gold standard. This change allowed currencies to be backed by government authority instead of physical goods.

How Modern Fiat Currency Systems Work

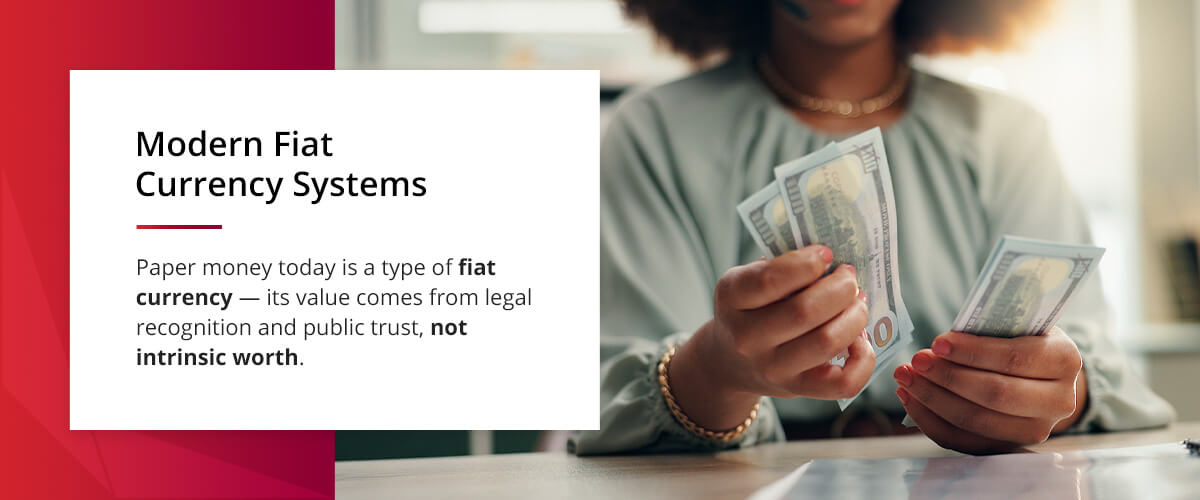

Paper money today is a type of fiat currency — its value comes from legal recognition and public trust, not intrinsic worth. Central banks regulate supply, interest rates and credit availability to manage economic growth and stability.

Fiat systems provide flexibility and efficiency, but they depend heavily on policy discipline — excessive printing can lead to inflation, eroding purchasing power over time.

The Case for Paper Money: Advantages of Fiat Currency

Despite criticism from gold supporters, the advantages of paper money can help explain its widespread use in modern economies.

Flexibility and Economic Control

Fiat currency is highly adaptable — central banks adjust supply to respond to crises and support large-scale economies. This flexibility allows modern economies to function at a scale that gold-backed systems could not support. For example, during the 2008 financial crisis or the 2020 pandemic, the Federal Reserve was able to inject trillions of dollars of liquidity into the system.

Practical Benefits for Daily Transactions

Paper money’s convenience powers daily purchases and digital transactions. For routine expenses like groceries, housing and services, fiat currency is essential. In contrast, gold is impractical for frequent use.

When Cash Outperforms Gold

In stable economic conditions with low inflation, paper money often performs well, providing liquidity, convenience and easy access. For short-term financial needs and situations requiring quick access to funds, cash is preferrable. Selling gold often involves transaction costs and delays, while cash provides immediate purchasing power. Cash equivalents can also earn interest, while physical gold does not generate income.

The Case for Gold: Why Precious Metals Endure

Gold remains popular due to features that fiat currency cannot imitate, especially for long-term wealth preservation.

Gold’s Track Record Against Inflation

Gold has proven effective as an inflation hedge over the long term. While its price can be volatile in the short term, gold has often maintained its purchasing power for very long periods, more consistently than most fiat currencies. This quality is one reason gold is often talked about as a hedge against inflation.

Protection During Economic Uncertainty

During economic stress, investors often see gold as a safe haven and move toward assets not directly tied to government-issued money.

Although gold does not generate income, its independence from monetary systems can make it appealing during uncertain times. Physical gold carries no counterparty risk, which is why central banks themselves continue to hoard it. According to the World Gold Council, 29% of central banks intended to increase their gold reserves before mid-2025, treating it as the ultimate safe haven.

Limited Supply vs. Unlimited Printing

In 2025, gold mining added roughly 2% to the global supply compared to the previous year. However, gold is a finite resource, while fiat currency supply can expand rapidly. This difference means fiat currency risks include the potential for devaluation, while gold’s limited supply helps resist inflation.

Side-by-Side Comparison: Gold vs. Paper Money

The table below highlights the key differences between gold and paper money in terms of usability, risk and long-term value.

| Feature | Gold | Paper Money |

|---|---|---|

| Liquidity | Less liquid | Highly liquid |

| Inflation hedge | Historically strong | Vulnerable |

| Government control | Minimal | High |

| Daily usability | Low | High |

| Long-term store of value | Historically consistent | Variable |

| Counterpart risk | None | Dependent on issuer |

This comparison shows why gold and paper money are often viewed as complementary rather than competing assets.

Real-World Performance: How Gold and Paper Money Have Fared

Theoretical advantages matter less than real performance. Looking at past results gives clear insight into how these forms of money compare.

Currency Devaluation Case Studies

Historically, many fiat currencies have seen significant devaluation due to inflation, debt or poor policy choices. From the hyperinflation of Venezuela to the collapse of the Zimbabwean dollar, paper money ultimately relies on confidence. When that confidence evaporates, value plunges to zero. While the U.S. dollar is the world reserve currency and unlikely to collapse overnight, it is not immune to the slow, steady bleed of devaluation caused by persistent inflation.

In these situations, gold often retained its value compared to weakened currencies, even if its nominal price fluctuated.

Gold’s Performance During Market Crashes

During financial crises, gold often outperforms stocks and currency-based assets. In 2008, as the S&P 500 index fell 30%, gold passed $1,000 per ounce, providing critical stability for diversified investors. As markets crashed in March 2020, gold quickly rebounded to new highs later that year, driven by the influx of stimulus money.

Purchasing Power Comparison Over Time

Over time, gold generally has preserved purchasing power, while paper currencies lose value due to inflation. This difference highlights why gold is commonly discussed in long-term financial planning.

In 1971, when the U.S. abandoned the gold standard, gold traded at $35 per ounce. Today, it trades above $2,000 per ounce, a nominal increase of over 5,600%. Over the same period, inflation has cut the dollar’s purchasing power by about 84%. While gold’s price gains have generally outpaced inflation over the long term, its value has also experienced periods of volatility and does not rise in a straight line.

Finding Balance: The Smart Approach to Gold and Cash

The question isn’t which is better in total, but how much of each makes sense for your situation and goals.

Determining Your Optimal Gold-to-Cash Ratio

Many investors keep 5%-15% of their investment portfolios in gold for diversification and crisis protection while maintaining liquidity for short-term expenses.

Your ideal allocation depends on several factors:

- Time horizon: Longer time frames favor more gold for inflation protection.

- Risk tolerance: Conservative investors may prefer more gold for stability.

- Income needs: Those who need regular withdrawals from their portfolio require enough cash.

- Economic outlook: Concerns about inflation or currency devaluation might justify increasing gold holdings.

Options for Adding Gold to Your Portfolio

You can add gold in several ways, each with its own benefits:

- Physical gold: Coins and bars need secure storage but offer maximum control and independence from financial institutions.

- Gold ETFs and mining stocks: ETFs and stocks are available through regular brokerage accounts, providing easier trading and liquidity.

- Self-directed IRAs (SDIRAs): SDIRAs let you hold physical gold in a tax-advantaged retirement account for additional diversification and tax benefits.

When to Increase Your Gold Position

Certain economic situations suggest raising gold allocations, for example:

- Rising inflation or expectations of future inflation.

- Concerns about currency devaluation or a weakening dollar.

- Geopolitical tensions that could disrupt markets.

- Central bank policies that significantly expand the money supply.

These conditions don’t guarantee that gold will appreciate, but they usually correlate with strong gold performance compared to paper currency.

Frequently Asked Questions

If you’re weighing gold versus paper money for your portfolio, you likely have questions. Here are answers to the most common concerns about both monetary forms.

- Is gold safer than cash in a bank? Both are safe in different ways. The Federal Deposit Insurance Corporation (FDIC) insures cash in a bank up to specific limits, protecting against bank failure, but not from inflation. Physical gold is not government-insured and requires secure storage, but it has historically held its value against inflation and currency declines.

- Can gold be held in a retirement account? Yes. Per IRS rules, certain precious metals can be held in self-directed retirement accounts.

- Can I switch my 401(k) to gold without paying taxes? Yes. By using a “rollover” into a self-directed IRA, you can move funds from a traditional retirement account into physical precious metals without triggering a taxable event or early withdrawal penalty.

- Why do governments prefer fiat currency? Fiat currency offers governments greater flexibility in managing economic growth and addressing crises.

Making the Right Choice for Your Financial Future

Gold and paper money each play important roles in today’s financial systems. Paper money supports everyday transactions and economic flexibility, while gold provides long-term value preservation and independence from monetary policy.

Rather than choosing one over the other, many people aim to understand how each asset performs under different circumstances. Knowledge, diversification and risk awareness are essential for navigating financial uncertainty.

Accuplan supports individuals who want to explore alternative assets, including gold, within self-directed retirement accounts while carefully following IRS rules.

Are you ready to explore gold investment options for your retirement? Fill out our application to begin, or call our experienced team to discuss how precious metals might fit into your wealth preservation strategy.

Our information shouldn ’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.